Synthetic intelligence (AI) pioneer Nvidia delivered an impressive quarterly report that crushed Wall Avenue’s expectations, sending shares of the chipmaker hovering because it turned clear that AI goes to stay a giant progress driver for the corporate. Nonetheless, Nvidia wasn’t the one semiconductor inventory that benefited from its spectacular displaying.

Shares of Superior Micro Units (NASDAQ: AMD) and Taiwan Semiconductor Manufacturing (NYSE: TSM), popularly often called TSMC, additionally loved a bounce following Nvidia’s report. Let’s examine why that was the case and examine why it might be price shopping for these two names straight away.

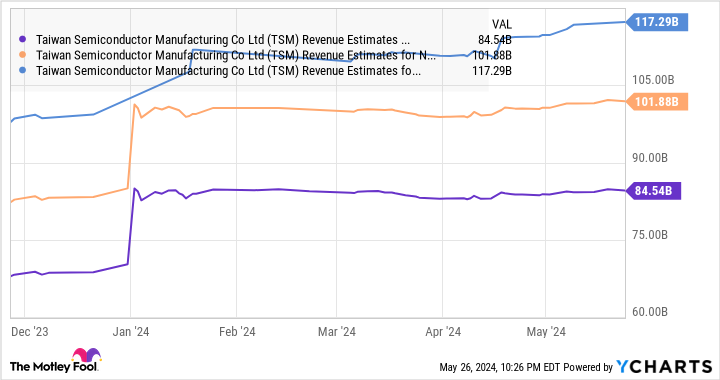

1. Taiwan Semiconductor Manufacturing

TSMC inventory jumped greater than 3% after Nvidia launched its earnings. That wasn’t stunning since Nvidia depends on TSMC’s foundries to churn out its AI chips. Nvidia is a fabless semiconductor firm, which implies that it solely designs chips; the manufacturing is finished by foundries equivalent to TSMC.

Nvidia is progressively changing into one in every of TSMC’s high clients. Although TSMC would not reveal particulars of its enterprise with particular person clients, Nvidia reportedly produced 11% of its high line final 12 months, in line with monetary analyst Dan Nystedt (by way of Tom’s {Hardware}). There’s a good likelihood that Nvidia is ready to contribute extra considerably to TSMC’s high line for a number of easy causes.

Nvidia administration identified on the corporate’s newest earnings convention name that it has introduced its next-generation Blackwell chips into full manufacturing already. The corporate will proceed to ramp up the manufacturing of its new chips within the fiscal third quarter. In keeping with third-party estimates, Nvidia may ship 420,000 items of its GB200 Blackwell Superchip, which incorporates two of the corporate’s newest technology B200 AI graphics processing items (GPUs).

Even higher, Nvidia is anticipated to ship between 1.5 million and a couple of million GB200 Superchips subsequent 12 months, which ought to pave the best way for terrific progress at TSMC. The preliminary manufacturing ramp-up of Nvidia’s new chips appears to be driving strong progress for TSMC already, as its income for April shot up practically 60% 12 months over 12 months, an acceleration over the 34% progress it had in March.

Extra importantly, TSMC is rising its manufacturing capability aggressively to satisfy the booming demand for Nvidia’s chips. The corporate not too long ago introduced that it’s set to extend its superior chip packaging capability — formally often called chip-on-wafer-on-substrate (CoWoS) — at an annual fee of 60% by means of 2026, not less than. This fast enchancment will enable TSMC to provide extra AI chips for Nvidia, which explains why analysts have been elevating their income progress expectations.

With TSMC presently buying and selling at 29 instances trailing earnings as in comparison with the U.S. expertise sector’s common of 42, traders are getting an excellent deal on this AI inventory, which they need to take into account grabbing with each palms earlier than it flies larger.

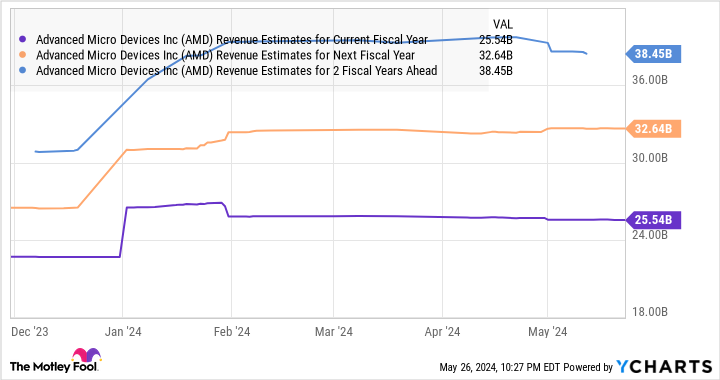

2. Superior Micro Units

Nvidia is the dominant power in AI chips with an estimated market share of greater than 90%. Because of this, the corporate has left little for friends equivalent to AMD, that are nonetheless struggling to realize a foothold on this profitable market.

For example, Nvidia’s information heart enterprise generated $22.6 billion in income due to the strong demand for its AI GPUs, a rise of 427% 12 months over 12 months.

AMD, then again, is forecasting simply $4 billion in income from AI GPUs for 2024. That pales compared to the income Nvidia generated in only a single quarter, however do not be stunned to see AMD ending the 12 months with stronger AI income than what’s presently anticipated. That is as a result of similar to Nvidia, even AMD is a key buyer for TSMC — reportedly accounting for 7% of TSMC’s high line in 2023.

So the Taiwanese foundry’s capability enlargement is prone to elevate AMD’s AI chip gross sales as nicely, particularly contemplating that the demand for its AI GPUs is strengthening, as CEO Lisa Su identified on the corporate’s April earnings convention name.

In keeping with the Taiwan-based Financial Every day Information, Nvidia and AMD have totally booked TSMC’s superior packaging capability for 2024 and 2025. AMD ought to be capable to procure and promote extra AI chips from TSMC because the latter aggressively lifts its manufacturing capability. Throw in added catalysts such because the rising demand for AI-enabled private computer systems and server CPUs, and it is not stunning to see why AMD’s progress is anticipated to stay wholesome over the following couple of years.

Even higher, analysts predict AMD’s earnings to extend at an annual fee of 33% for the following 5 years. And it may ship stronger progress if it manages to seize an even bigger share of the AI chip market.

Analyst Harsh Kumar of Piper Sandler factors out that AMD has traditionally performed second fiddle to Nvidia in markets equivalent to PC graphics playing cards, with a share of 20% to 30%.

The same share in AI chips might be a giant deal for AMD in the long term contemplating that this area is anticipated to generate $384 billion in 2032, rising at an annual fee of 38%, which is why it is likely to be a good suggestion to purchase this tech inventory earlier than it goes on an AI-fueled rally.

Must you make investments $1,000 in Taiwan Semiconductor Manufacturing proper now?

Before you purchase inventory in Taiwan Semiconductor Manufacturing, take into account this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Taiwan Semiconductor Manufacturing wasn’t one in every of them. The ten shares that made the minimize may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… when you invested $1,000 on the time of our suggestion, you’d have $677,040!*

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of Could 28, 2024

Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Units, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot has a disclosure coverage.

2 Prime Synthetic Intelligence (AI) Shares to Purchase Following Nvidia’s Blockbuster Earnings was initially revealed by The Motley Idiot

{kind=link}